India and the United States share one of the world’s most dynamic and rapidly expanding air cargo corridors, underpinned by deepening commercial ties and the movement of high-value, time-sensitive goods.

Recent data underscores the resilience of this lane. India’s air cargo exports to the United States rose by 15 per cent year-on-year during the week of January 19–25, 2026, extending the strong momentum seen in the closing months of 2025, according to WorldACD’s Weekly Air Cargo Trends. This growth has come despite higher US tariffs introduced in the second half of last year, highlighting not only the robustness of India–US trade flows but also the sustained demand for Indian pharmaceuticals, electronics, engineering goods, and e-commerce shipments that rely heavily on air transport.

WorldACD further noted that while volumes from Asia-Pacific to the US and Europe flattened in week four after two weeks of strong recovery, shipments to Europe remained ahead of last year’s levels. Flows to the US were only marginally lower year-on-year for the broader region, even as India-origin traffic continued to outperform. For Indian exporters, these trends suggest that despite tariff-related headwinds, capacity rebalancing, and geopolitical uncertainty, the India–US air cargo corridor continues to offer reliable uplift and pricing support for critical product categories that cannot tolerate long transit times.

Pertinently, the Airforwarders Association (AfA) has welcomed recent trade-related developments between India and the US, viewing tariff rationalisation as a positive signal for global supply chains. AfA has consistently underlined that predictable and transparent trade policies are essential for sustaining investment in logistics infrastructure and maintaining confidence across international freight networks. Reduced friction at borders, the association notes, directly benefits exporters, logistics service providers, and end consumers by stabilising costs and improving delivery timelines.

In parallel, the announcement of an India–European Union trade agreement marks a significant inflection point for global trade, not merely because of its scale but due to what it signals about the future direction of supply chains. As trade becomes more regionalised and resilience-driven, the agreement reinforces the need for integrated transport solutions that combine air, sea, rail, and road networks. Industry leaders have emphasised that capturing the full value of such agreements will depend on how effectively countries and logistics providers move beyond traditional port-to-port or airport-to-airport models toward end-to-end, multimodal connectivity.

India’s Cargo Ecosystem at an Inflection Point

Against this backdrop, India’s cargo and logistics sector is undergoing a profound transformation. Record-breaking volumes at major ports, a fast-growing air freight market, sustained investments in airport and hinterland infrastructure, and a strategic shift toward digitisation are reshaping the country’s logistics landscape. This evolution is being driven by the ‘Make in India’ initiative, the explosive growth of e-commerce, rising pharmaceutical and electronics manufacturing, and the imperative to build supply chain resilience amid ongoing geopolitical disruptions.

Fresh weekly data reveals a 15 per cent year-on-year surge in India-US air cargo exports, underscoring the immediate boost from recent bilateral trade developments. The Airforwarders Association has welcomed the tariff rationalisation, highlighting its role in stabilising supply chains for critical pharma and electronics exports, even amidst broader geopolitical uncertainty

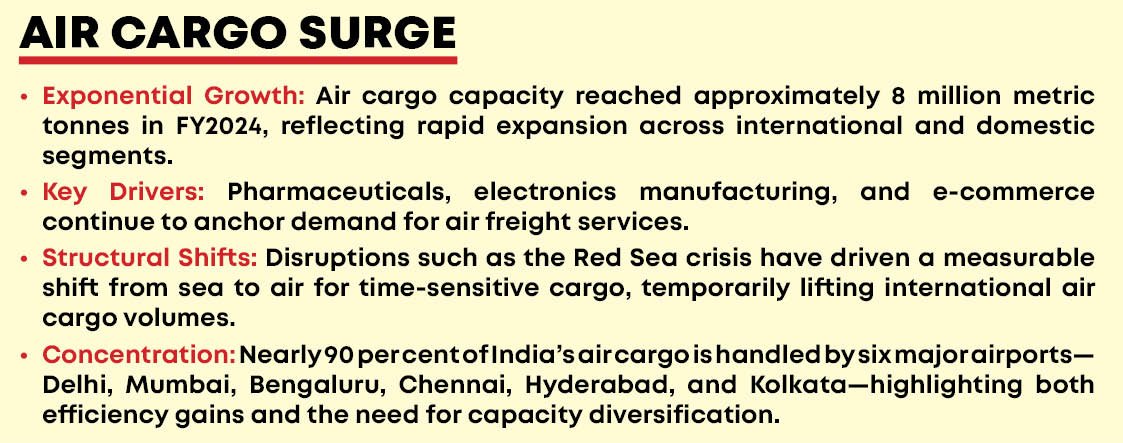

Air cargo, in particular, has emerged as a critical enabler of India’s trade ambitions. Handling capacity touched approximately 8 million metric tonnes in FY2024, reflecting the rapid expansion of both international and domestic cargo operations. While projections vary across agencies, the underlying trajectory points to sustained growth through the second half of the decade, fuelled by pharmaceuticals, electronics, high-value engineering goods, and express shipments.

The Red Sea crisis has further accelerated a modal shift from sea to air for time-sensitive cargo, temporarily boosting international air freight volumes and reinforcing the strategic importance of air cargo capacity.

In this context, upcoming infrastructure such as the proposed air cargo terminal at Vadhavan assumes strategic significance. Conceived as part of India’s first offshore airport and aligned with the PM Gati Shakti National Master Plan, the terminal reflects a well-thought-out effort to synchronise air, sea, road, and rail connectivity. By enabling seamless transfers between maritime gateways and air cargo facilities, such projects aim to reduce logistics costs, which in India remain higher than the global average, and to improve the speed and reliability of export-import movements across South Asia.

Hubs, Carriers and the Push for Multimodal Integration

At present, India’s air cargo volumes are concentrated across a limited number of major hubs, which together handle roughly 70–75 per cent of the country’s total throughput.

Delhi’s Indira Gandhi International Airport stands as the largest cargo gateway, handling over one million metric tonnes annually. Its specialised Transhipment Excellence Centre and the country’s largest on-airport temperature-controlled facilities make it a preferred hub for pharmaceuticals, perishables, and high-value transhipment cargo.

Mumbai’s Chhatrapati Shivaji Maharaj International Airport remains a critical gateway for general cargo and perishables, though it continues to face capacity constraints.

Bengaluru’s Kempegowda International Airport has emerged as a key southern hub, driven by strong growth in electronics and engineering exports.

Hyderabad’s Rajiv Gandhi International Airport has positioned itself as a global pharmaceutical powerhouse, with pharma accounting for nearly 72 per cent of its cargo volumes and supported by dedicated cool port infrastructure for vaccines and biologics.

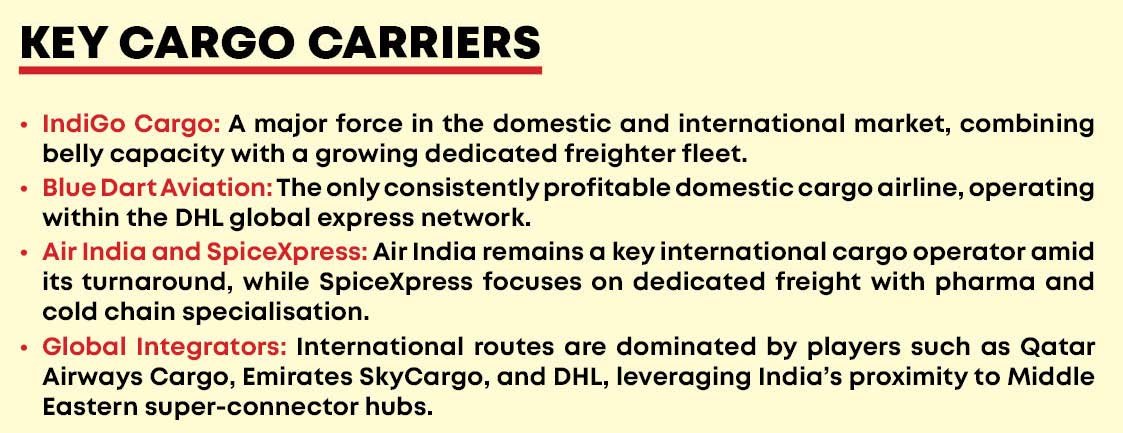

On the carrier side, India’s cargo market presents a blend of dedicated freighter operators and passenger airlines with substantial belly-hold capacity. IndiGo Cargo, the freight arm of India’s largest airline, has rapidly scaled operations, handling around 400,000 tonnes through a combination of belly cargo and a growing fleet of Airbus A321P2F freighters. Blue Dart Aviation remains the only domestic cargo carrier to report consistent profitability, underpinned by long-term, time-definite contracts within the DHL global network.

Air India, currently in a phase of transformation under new ownership, continues to be a significant international cargo player, while SpiceXpress operates as a dedicated cargo entity with specialised capabilities in pharmaceuticals and cold chain logistics.

Strengthening regional and international connectivity further, operators such as Quikjet Cargo Airlines are expanding dedicated freighter services linking Northeast India with Southeast Asian markets. Routes connecting Guwahati to Hanoi and onward to Delhi, operated using Boeing 737-800BCF aircraft, are designed to support faster and more reliable cargo movement for time-critical shipments, enhancing the integration of India’s northeastern region into global supply chains.

The broader cargo ecosystem is also being reshaped by policy and institutional initiatives. India has entered an era where geopolitical volatility is no longer an exception but a defining operating condition for global trade.

The newly announced India-EU trade agreement is accelerating investments in multimodal nodes, like the planned Vadhavan air cargo terminal, designed to seamlessly connect air and maritime gateways and capitalise on the agreement’s potential by reducing logistics costs and improving speed

Policymakers have repeatedly stressed that as India aspires to become a major global aviation hub, it cannot remain dependent on external suppliers for critical aviation and logistics capabilities. In line with this vision, the government is promoting Gati Shakti Multi-Modal Cargo Terminals, with 118 of the planned 306 terminals already operational. These facilities are intended to serve as nodes of integration, linking industrial clusters, ports, airports, and consumption centres through a unified logistics grid.

Together, these developments position Indian air cargo as a central pillar of the country’s multimodal trade strategy. As infrastructure, policy, and industry capabilities converge, air cargo is set to play an increasingly decisive role in shaping India’s integration into resilient, high-value global supply chains.

The author retired as a Senior Technical Officer at the Central Salt and Marine Chemicals Research Institute, Bhavnagar (Gujarat), and currently contributes articles to research journals and magazines. The views expressed are personal and do not necessarily carry the views of Raksha Anirveda.